Allianz Trade Corporate Advantage

Customer Service Guide

What can I do via the Online Service?

We have agreed in your policy which customers you can get cover on.

Yes, there are some exceptions. You can find what is not insurable in the General Conditions of Insurance (GCI) Section A.4.

For instance, the payment term you grant your Buyer must not be longer than the “Maximum Terms of Payment” fixed in the Schedule to your policy. And you must have sent an invoice within 30 days after delivering the goods or performing the services.

Receivables are also not insured, for instance, if your Buyer belongs to one of the following categories:

• public buyers, e.g. the Federal Government, regional or municipal governments.

• Private individuals acting in their own capacity.

• Your own associated companies.

Value-added tax and other similar sales and energy taxes are also not insured.

Important: there may be exceptions to these rules if you have agreed special provisions in your policy or in supplementary clauses. Thus, for example, business with private individuals or withdrawals from consignment stocks can be covered.

1. To request your full customer list, select the contact option in the quick menu in the upper right corner.

2. Click "Create a new message". A contact window will open.

3. Under "Subject", select "Policy/ Administrative". Then select your Policy.

4. Please send us your message via the "Title" and the "Comment". e.g. "Please send customer list". If you would like to receive your full customer list regularly, e.g. on a weekly/monthly basis please let us know.

Note: You have the option to receive a confirmation by email and to be notified about the answer.

5. Click on "Send my message". You will receive a confirmation and then you can view your message.

6. The status of the message will change as soon as your request is processed.

Simplify your day-to-day work – and keep full cover on your “small” customers at the same time.

You can set a credit limit on a Buyer yourself up to the maximum amount defined as the Discretionary Limit, e.g. if:

• your Buyer has received deliveries of goods or you have provided services to them at least twice during the past 12 months and these have been paid on the originally agreed due date or by the Maximum Extension Period (see Station 5) or

• you have received a written credit report from a bank or a credit information agency approved by us on your Buyer which is no older than 12 months justifying the amount of credit you wish to grant by specifying an appropriate maximum credit limit amount.

You can find the details for this in the clause “Conditions for granting cover within the Discretionary Facility”.

Please note: you may in general not set a discretionary credit limit on a Buyer if you have information on your Buyer’s financial situation or have become aware of any circumstances during the past 12 months which would exclude the granting of credit.

If discretionary cover is not the right solution for you, Allianz Trade will carry out the credit check. You need to submit a Credit Limit Request on every new buyer in the agreed countries to have them included in cover.

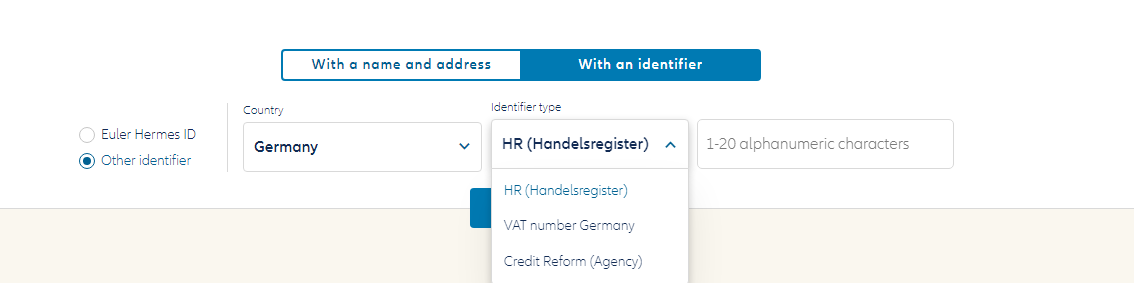

1. Select "Dashboard" in the quick menu in the upper left corner to access the credit decisions. From there, select your customer.

2. Search either the company name and address or the identification number. Click on "Search".

Then select the customer.

3. Now select the desired contract under "My policies". And click on "New Request". Enter the desired credit limit in the "Amount" field and confirm.

Additional information: Through the import function, you can make multiple credit requests together. You can find detailed information here.

1. Select the "Customer Overview" in the quick menu in the upper left corner to access the "Risk services". Select your customer there.

2. Select "Reduce" in the status area.

3. Check the information for correctness and confirm the deletion of the insured amount.

Additional information: Through the import function, you can reduce multiple credits together . You can find a detailed information here.

1. Select the "Customer Overview" in the quick menu in the upper left corner to access the "Risk services". Select your customer there.

2. Select "Cancel" in the status area.

3. Check the information for correctness and confirm the deletion of the insured amount.

Additional information: If you want to cancel several credit limits at once, you can use the function "Mass actions". You can do so by simply selecting the credit limits that you want to cancel within your client list and clicking on "Cancel limit". To request, edit or reduce several credit limits at once, please find more information about mass imports in the next question.

With the mass import function you can edit several credit limits at once. Please find more detailed information in the following guides:

Guide to import - Cancel

Guide to import - Reduction

Guide to import - Credit request

Guide to import - Customer reference update

Please make a credit limit request within 30 days of the Declaration Limit being exceeded by the newly accrued receivables.

And by the way: under the clause “Cover for existing receivables” a credit limit is valid for all receivables which are no older than 30 days at the time the credit limit request is submitted, irrespective of the date of validity on the credit limit notification.

• When you apply for inclusion of a buyer, you are asking us to set a credit limit on them.

• We check the buyer’s creditworthiness and you will then receive a credit limit notification.

• This credit limit notification contains the credit limit and, where appropriate, further information and specifications in connection with your cover.

• Before you fill in the form, please check exactly who is your payer, i.e., who is liable to settle the outstanding receivable.

• We can only assume credit limits for legally independent entities at their registered Head Office. Receivables due from legally dependent branches, sales offices or permanent business establishments are always insured via their parent company.

• When you decide the amount of the credit limit you wish to request, please remember that our indemnifications during one and the same insurance year are always limited to the level of the so-called Maximum Liability.

• Please make sure to complete your request in full. Remember that we can only begin a check on your enquired company when all the information necessary has reached us.

• Please do not forget to answer all the questions on your experience with your buyer’s payment behaviour, in order not to jeopardize any possible later indemnification.

Always when there is no cover under your Discretionary Facility for the goods you want to deliver or the services you want to perform.

Please submit your Credit Limit request as early as possible so that you are clear whether you have cover before you deliver the goods or perform the services. If you only submit the Credit Limit request after delivery or performance and we approve the Credit Limit, cover is valid retroactively from the commencement of the policy and includes receivables which have already accrued.

• Before you fill in the form, please check exactly who is your payer, i.e., who is liable to settle the outstanding receivable.

• We can only assume credit limits for legally independent entities at their registered Head Office. Receivables due from legally dependent branches, sales offices or permanent business establishments are always insured via their parent company at their registered Head Office.

Our tip: check your Approved Credit Limits regularly. Delete them when you no longer need them. That way you save on monitoring fees.

• When you decide the amount of the credit limit you wish to request, please remember that our indemnifications during one and the same insurance year are always limited to the level of the so-called Maximum Liability. This may be either a fixed amount or a multiple of your premium.

• Please make sure to complete your request in full. Remember that we can only begin a check on your enquired company when all the information necessary has reached us.

• In particular, please do not forget to answer all the questions on your experience with your Buyer’s payment behaviour as accurately as possible, in order not to jeopardize any possible later indemnification.

• We check your Buyer’s creditworthiness.

• We make a credit limit decision.

• You receive a Credit Limit Notification.

We will tell you more about what is in the Credit Limit notification at the next stop.

If your premium is turnover-based and your policy does not include a discretionary facility, this is not a breach of your obligations under the policy. But you may not omit receivables from this Buyer when you declare your turnover for premium calculation, even though you have no cover on them.

If you pay premium based on outstandings, it is vital that you should do everything you can to obtain cover. Otherwise your cover may be jeopardized.

When we make a credit limit decision, you will receive a written Credit Limit notification.

The following decisions are possible:

Full acceptance

Partial acceptance

Provisional acceptance

Refusal

Interim notification

The following credit limit decisions are also possible in respect of existing credit limits:

Withdrawal

Reduction by us

We can only grant cover for future deliveries in a lower amount

As a rule, you have 30 days after receiving notice of the withdrawal, reduction or other changes in cover to carry out deliveries of goods or performance of services. This does not apply, however, if your Buyer is already in a State of Default.

The due date is a milestone in every business relationship. If it is missed, caution is called for.

1. Download the form for Notification of the impending default of your buyer from the library. Fill in the form and save it.

2. Go to Allianz Trade Online and then go to the contact function.

3. Select "Create a new message". And select "Credit" as the subject and click on your policy. Also enter the EH ID of the customer.

4. Fill in the required fields and upload the completed form.

Note: You can have a confirmation of receipt sent to you by email.

You can use the contact option on Allianz Trade Online to have your payment receipt confirmed as a message.

It describes the situation of a Buyer if:

• The Buyer is insolvent;

• An overdue amount has not been paid at the expiry of the Maximum Extension Period;

• A direct debit has been returned due to lack of funds on the Buyer’s account;

• You have received information about your Buyer’s ability to pay which leads you to believe that they will probably not be able to pay your receivable as and when it falls due.

When your Buyer is in a State of Default, this marks a watershed moment which has certain consequences, and means that you need to take certain steps:

• With immediate effect, further deliveries of goods or performance of services are no longer covered;

• If the overdue payment is still not paid after 15 days, you must submit a “Notification of an overdue account” to us. The best way to do this is via the Online Service.

• Instead of an overdue report, you can also immediately submit the Claims & Collection Form (C&C Form) if you think that an event of loss is imminent.

And by the way, this also applies if your Buyer is covered under your Discretionary Facility.

In your own interests, please take your contractual duties of notification seriously.

We all know that the risks in the market are constantly changing. To make sure that your insurance cover remains in full force and effect, please observe the following obligations to notify any relevant risk information to us.

Wischen um mehr anzuzeigen

|

Event

|

Duty to notify?

|

|---|---|

| Non-payment on due date |

No |

| Non-payment of undisputed receivables at the expiry of the Maximum Extension Period | Yes, “Notification of a State of Default” of your Buyer within a deadline of 15 days |

| Non-payment of undisputed receivables at the expiry of a payment term extended by you with our consent if the extended due date is later than the expiry of the Maximum Extension Period | Yes, “Notification of a State of Default” of your Buyer within a deadline of 15 days |

| Non-payment of disputed receivables | Yes, but first as a claim notification using the “C&C Form” before expiry of the deadline for claim notification |

| Insolvency | Yes, “Notification of a State of Default” of your Buyer within a deadline of 15 days and claim notification within 30 days |

| Direct debit returned due to lack of funds | Yes, “Notification of a State of Default” of your Buyer within a deadline of 15 days |

| Negative information which leads you to believe that your Buyer will probably not be able to pay your receivable as and when it falls due | Yes, “Notification of a State of Default” of your Buyer within a deadline of 15 days |

| You have granted your Buyer an extension of due date or agreed to payment in instalments or deferred payments with expected payment in full before the expiry of the Maximum Extension Period. | No prior consent from us needed |

| You have granted your Buyer an extension of due date or agreed to payment in instalments or deferred payments with expected payment in full later than the expiry of the Maximum Extension Period. | Only with our prior consent |

| Non-payment at expiry of the deadline for claim notification | Yes, “C&C Form” must be received by us at the latest at expiry of the deadline for claim notification |

This station of your journey only contains your obligations under the GCI.

Further obligations concerning what you need to notify us of and when may apply however under special clauses we have agreed with you.

And of course there is the duty to notify us for the calculation of your premium.

You can agree extended conditions with your Buyer subsequently without needing to obtain our consent. The important thing to observe is only that such agreements must envisage the payment of your receivables in full at the latest by the expiry of the Maximum Extension Period.

If you want to grant your Buyer subsequently altered payment conditions exceeding the Maximum Extension Period, however, you need to obtain our prior consent to this.

If the reason for your Buyer’s State of Default subsequently no longer applies, e.g. because he later takes the overdue payment, cover will be reinstated with retroactive effect.

Exception: if we have withdrawn, reduced or changed the Approved Credit Limit in the meantime or an Event of Loss has already occurred.

Your premium is calculated on the declarations you make. You can read here how that works.

1. Please select "turnover/ outstandings declaration" via the point grid "AppLauncher" in the menu in the upper right corner. It will open in a new window in your browser.

Note: Please make sure that pop-ups are allowed in your browser settings.

2. Click "Declare" for the relevant period and policy to declare your turnover/ outstandings.

3. Please enter your total and uninsured turnover/outstandings. There are usefull information stored in headlines to support you with the calculation.

4. Click on "Submit" and confirm your declaration.

5. The status of the declaration changes from "To do" to "Done". You cannot change your declaration afterwards.

If you need to change a declaration please contact us by Email or with the contact feature in Allianz Trade online.

In premium on turnover, the premium payable is calculated on the basis of the “actual” turnover you make during the insurance year.

How do I tell the difference between “insured” and “uninsured” turnover?

The basis for calculating the figure is your total turnover with Buyers in the insured countries.

From this, you can deduct:

• receivables which are not insured according to Section A.4. GCI, e.g. those due from public buyers or your own associated companies;

• VAT or comparable sales or energy tax.

You may also omit turnover with Buyers for whom we have completely refused or have withdrawn cover in a Credit Notification.

In premium on outstandings, the premium payable is calculated on the basis of your outstanding insured receivables.

How do I calculate what outstanding amounts I need to declare?

The basis for calculation is the receivables which are still unpaid on the last day of each month. You may omit receivables due from Buyers on whom you have no cover because we have completely refused or have withdrawn cover in a Credit Notification.

If you have applied for an Approved Limit which was sufficiently high, but for which we have only granted a partial amount, you may also omit the part of the receivables in excess of the existing Approved Limit.

In order to calculate the “outstandings” to be declared, you may also omit the following:

• receivables which are not insured according to Section A.4. GCI, e.g. those due from public buyers or your own associated companies;

• VAT or comparable sales or energy tax.

When a loss occurs, we are there for you – as soon as we know about it! You can find here the most important things you need to know about an event of loss.

1. Select "Non-Payment" in the "Main menu" on the left to report a claim or collection. Then click on "Declare a non-payment".

Choose between the options "I already have cover on the debtor " or "I don’t have cover on the debtor yet/ I don’t know" and search for your debtor by identification number or by name and address. Then select your debtor.

Note: You can also search for your debtor by the HR number; VAT number or Creditreform.

2. In the next step select “submit a claim/collection” and enter all the information about your claim, as well as the contact at the debtor.

3. Now select the type of claim and enter the corresponding data. You can attach several invoices. In addition, you can optionally store a comment.

4. In the next step you have the possibility to attach documents. Documents to be submitted are displayed on the left side.

5. Then create a contact person for the claim.

6. In the last step you have to confirm that all information is true and send the notification.

When:

• a (provisional) insolvency administrator or a (provisional) trustee is appointed;

• the court has rejected the opening of insolvency proceedings for lack of assets;

• the insolvency court has formally noted that a plan for the repayment of creditors in a personal insolvency has been accepted;

• all the Buyer’s creditors generally have agreed to a composition or out-of-court settlement (voluntary liquidation or quota settlement);

• the execution of a judgement title obtained by you in respect of the Buyer’s assets has failed to satisfy the debt in whole and this has been confirmed in writing by the bailiff.

You must have submitted the “Claims and Collection Form” at the latest by the expiry of the claims notification deadline specified in the Schedule to your policy. If the Buyer is not already formally deemed to be in insolvency, the period starts as a rule after the Maximum Extension Period has expired.

Please read the explanations on the C&C Form through carefully and answer all the questions in detail – otherwise we will not be able to process your information without calling you back, which causes delays.

In general, make sure to secure your claims against your Buyer as soon as possible, e.g. by asserting your rights under the retention of title you have agreed with them. Lodge your claims in the insolvency schedule in plenty of time.

Before undertaking any further measures against your Buyer, coordinate these with us and our collection provider Allianz Trade Collections.

Important: The event of loss must have occurred during the Policy Period!

All your receivables safely under control – with our debt collection service.

• You place a collection order when you send the “C&C Form”.

• The quickest and simplest way is via our Online Service.

• Please submit the required documentation at the same time.